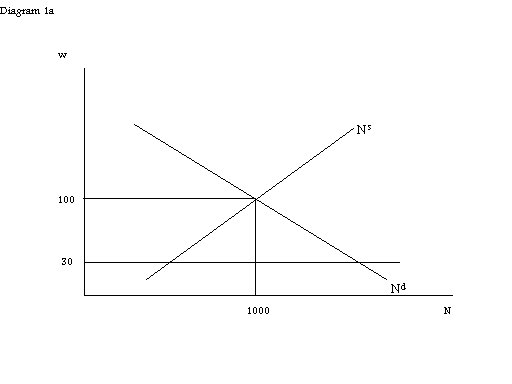

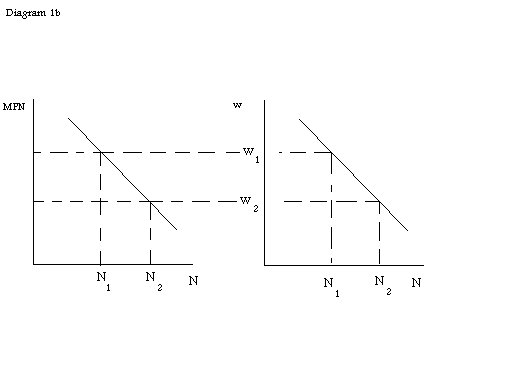

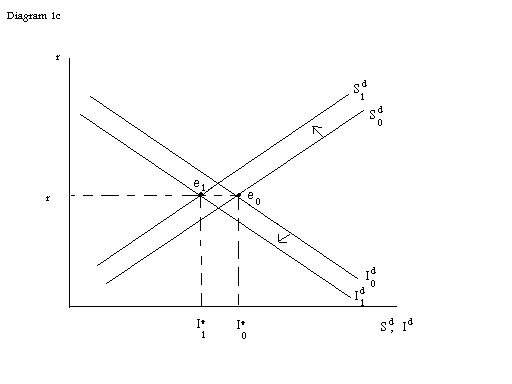

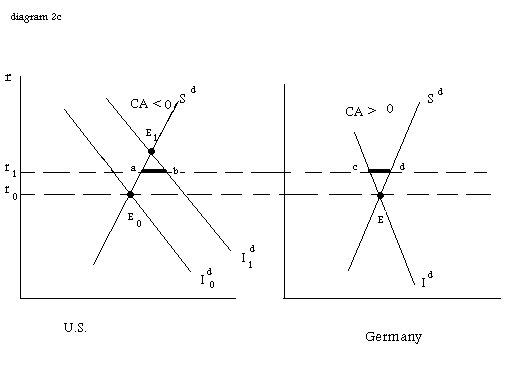

Part I (For this section students were responsible for doing 5 out of 7 questions only. Therefore marks were granted for only five questions attempted additional questions are not marked) 1. (a) Inflation rate = price index 1999 price index for 1998 (assuming this is the base) Variable weight price index = QcurrentP current QcurrentPbasePrice index 1999 = value of 1999 output at 1999 prices * 100 = 114.5 value of 1999 output at 1998 prices-> inflation rate = 14.5% (approximate) -> Even though the price of chocolate has fallen, the aggregate price level is higher due to the increase in the price of bread which receives a higher weight in the calculation.(b) GDP deflator = variable weight price index = x Solve the following equation : inflation rate % = (x- price index 1999)/price index 1999 0.05= (x-114.5)/114.5 => x=120.225 (approximate is fine)2. GDP = value of final goods and services Rules : 1. Inventories are valued at cost of production 2. Fertilizer is treated as an intermediate input value of final goods: Hats (4000*1.00+1000*0.50) = $4500 Fish $30,000-$5000 = $25,000 Wheat $50,000 GDP = 79,5003. Uncertain: Statement is true if the economy is a closed one. Government savings must finance any excess of investment over private savings. However, in the case of an open economy, investors can borrow from the international market therefore it is not necessarily true that government must run surplus. In fact, the government can also run a budget deficit, and both could borrow in the international market. In which case, the statement can be true or false. Therefore, the answer at best is uncertain. All of the above is evident in the uses-of-saving equation: Spvt = I + (-Sgovt) + CA Spvt-I = (-Sgovt) + CA Note: -Sgovt is deficit, Sgovt is surplus.4. (a) 0 because the steel is an intermediate good (b)$200 only commission is counted because it is a current service. The antique was not produced in the current year. (c) 0, no activity generated, simply a transfer of funds (d) 50,000, a fall in inventories is a change in inventories that will reduce GDP one to one.5. An increase in capital stock implies that (a) output will be higher, (b) lead to an increase in the marginal product of labour, which will shift the labour demand rightward, causing real wage and employment to rise, which will cause output to rise. Full employment output is determined by market clearing employment level. An increase in N will therefore cause full-employment output to increase. An increase in capital will also directly increase the output as well => there are two channels at work.6. An increase in expected inflation will reduce real interest rate, causing a substitution effect and an income effect. According to the substitution effect, the individual will reduce savings since the price has fallen. According to the income effect, savings will increase. The impact on savings depends upon the relative strength of these two effects. If the substitution effect dominates, then savings will fall as a result of an increase in expected inflation. If the income effect dominates then savings will rise.7. False: Current account + capital account = 0 If current account is negative 5 million, this implies that the capital account _is_ + 5 million. However, the CA<0 and KA>0 implies that that the country is net BORROWER. A positive capital account implies an inflow of Canadian dollars => either we disposed off foreign assets or we borrowed from foreigners who now hold domestic assets. In either case, country is a net borrower and not net lender.Part II(i) equilibrium condition: Sd= Y - Cd - G = Id Substituting Y=5000, G=1000 and the formula in the problem, 5000 - (3000 + (0.9*0.5*5000) - 20000r) - 1000 = 1000 - 40000r. Then r = 0.0375 and Sd = Id = -500.(ii) Substituting r=0.05, Id = 1000 - (40000*0.05) = -1000. Sd = 1000 - (0.9*0.5*5000) + (20000*0.05) = -250. By the formula Sd = Id + CA, the country has a current account profit 750.(iii) (a) Desirable investment is determined by MPKf = UC/(1-tau) When the revenue tax tau increases, firm decreases desirable capital stock at the next period, and hence reduces Id. Since Id shifts left, which will result in lower interest and lower Sd=Id.(b) Increase in government purchase decreases disposable income of the household, and hence the desirable saving decreases (6). As a result, we have lower Sd=Id and higher interest rate, r.Notes: I. Those who mentioned aggregate demand or aggregate supply are not correct. It is worth mentioning that goods market determines r and not P (P is determined in the money market: see Section 7.4 and 9.4). II. For those who explained labor market equilibrium, full marks were granted only when the explanation was reasonable. However, we assume at the beginning of section 3.2 that change in K is supposed to be small in the short run, and hence the decline in K in question (a) does not have a large impact on MPN. So the impact on the labor market is negligible (or zero, if we consider at the beginning of the year of the tax change). III. For (b), Ricardian equivalence does NOT matter. Ricardian equivalence is about TAX change and NOT about government spending change.Part IIIQ1. (a) MPN = 1000 - 0.9N Ns = 400 + 8(1-t)w Demand condition: w = MPN, so: w = 1000 - 0.9N d Supply with taxes subbed in: Ns = 400 + 8(0.75)w = 400 + 6wEquilibrium: Labour Supply equals labour demand. Can either rearrange demand equation such that N is on the LHS and all other variables and numbers are on the RHS and then equate Nd with Ns. An alternative solution method is simply to sub the demand equation into the Ns equation as follows:N = 400 + 6(1000 - 0.9N) note here that Ns= Ns in eq'mSo then N* = 1000 and we can solve for w by subbing the value of N back into either the labour demand or the labour supply equation. w* = 1000 - 0.9(1000) = 100 If real wage is set at 30, the firm would want to hire more workers, but the labourers will want to hire less. Since it is below the market clearing wage, there is an excess demand for labour. There is no increase in unemployment, so setting w=30 has no impact as it is below market clearing wage. (see diagram 1a)(b) Diminishing returns implies that MPN is downward sloping because as more and more labour units are added to fixed capital, the contribution of labour units delines. Firms hire labour to maximize profits. The profit maximizing condition is hire until MPN = w. Therefore, since MPN is downward sloping, the labour demand curve is also downward sloping. (see diagram 1b)(c) In a closed economy, the equilibrium condition is: Sd= Id A permanent increase in gasoline price will have two effects:i) MPKf will decrease which will cause desired capital stock, K, to decrease. Therefure Investment demand, Id, will decrease. (future MPN will be lower because of the decrease in MPK as well) ii) MPN will decrease which implies real wages and equilibrium employment levels will decrease. In turn, this will cause future output to decrease. As such consumption and savings will decrease. Productivity, A, will also decrease, causing future output to decrease. So consumption and savings will decrease further.So the savings curve will shift up and to the left, while the investment curve will shift down and to the left (see diagram 1c) Therefore, the effect on the equilibrium value of r is ambiguous, but the effect on desired savings and investment is clear, they both decrease. (Note: temporary effect implies only Sd will shift, and therefore equilibrium r will clearly rise. However, when the effect is permanent, Id shifts as well, making the equilibrium effect on r ambiguous)Q2. (a) Tax adjusted User Cost of Capital = UC/(1-tau) = (r + d)Pk/(1-tau) = (0.1 + 0.1)(10,000) = 4000 1-0.5 The firm determines the optimal amout of K to purchase by equating MPK with the tax adjusted user cost of capital (MPK = UC/(1-tau)): 5000-2K = 4000 K* = 500(b) Ricardian Equivalence implies that a temporary change in taxes, holding current and future spending by the government constant, will have no impact on current consumption, therefore current aggregate savings. Individuals will percieve a tax cut today as implying a higher tax at some future date, and therefore any tendency to increase consumption demand today wil be cancelled out by a tendency to decrease consumption demand in order to save for future tax hikes.(c) (see diagram 2c) An increase in MPKf in the U.S. will cause the amount of capital desired to increase. So Id in the U.S. will increase (the I curve will shift right and up). Initially the economy is in equilibrium at ro. No surplus or deficit. After the U.S. has a shift in I, ro is no longer the equilibrium world interest rate as CAu.s. is less than zero (deficit), but CAG = 0, as such CAu.s. does not = - CAG, so the world is not in equilibrium. In order to reach the new equilibrium, r must rise. The new equilibrium value is r1, where the U.S. has a CA deficit (ab) and germany has a CA surplus (cd) where ab=cd. Intuitatively, excess demand for funds (investment) in the U.S. causes the world r to be bid up. However, the rising r encourages savings in the U.S. and Germany, but discourages investment in both countries. And r will continue having these effects until the new equilibrium is attained.

DIAGRAMS BELOW

{kind=link}

{kind=link}

{kind=link}

{kind=link}